Fed’s Policy Tightrope, Recession Rumbles, and AI Mega-Cap Dominance

Markets head into the 39th week of 2025, historically the weakest week of the year, with a rare mix of dovish Fed expectations, growing recession fears, and relentless AI-driven market leadership.

While indices continue their upward grind, traders face a complex landscape: rising stagflation concerns, looming government shutdown threats, and heightened seasonality risks. With October just ahead, the stage is set for either a consolidation phase or a volatile rotation across sectors.

Market Overview – “Uptrend With a Pause Button”

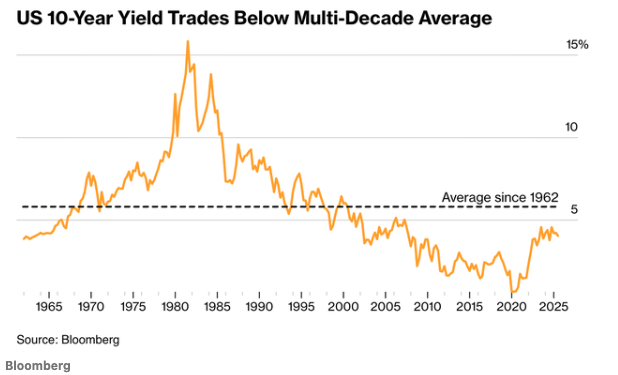

US equities have “shot off into the sky” but are now brushing up against several headwinds — the government shutdown threat, US10Y yield spikes, and inflation creeping back into the stagflation narrative. Seasonality has been delayed all year, yet October looms as the likely month for consolidation. The parallels to Q4 2018 are striking — Trump wrestling with inflation optics and a softening jobs market even as tech carries the index weight.

Retail flows remain robust, but the real question is whether institutions are the marginal buyers or if the “risk-on” bid fades. The AI/commodities/value cyclicals trade remains dominant, but a multi-entry point setup is emerging for equity traders.

Macro & Policy Watch: Fed vs. Trump and the Third Mandate

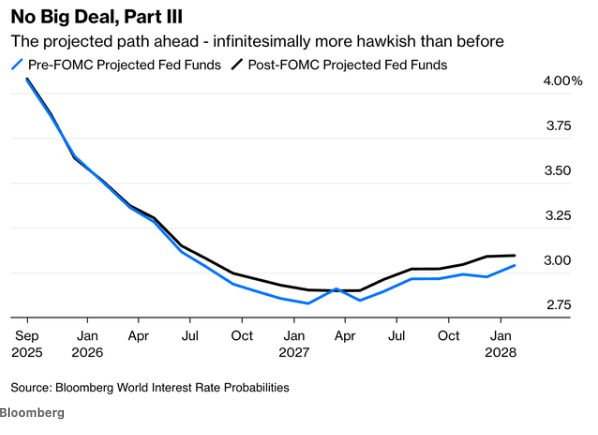

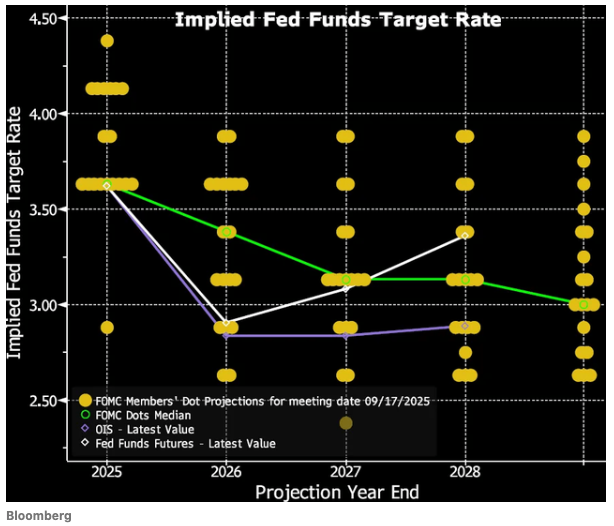

The Fed is attempting a high-wire act: delivering insurance cuts while inflation remains stubbornly elevated. The latest dot plot highlights the internal divide: one member called for a hike, another for a 50bps cut, and the rest split across a wide spectrum — the broadest policy divergence in years.

Economic signals remain mixed:

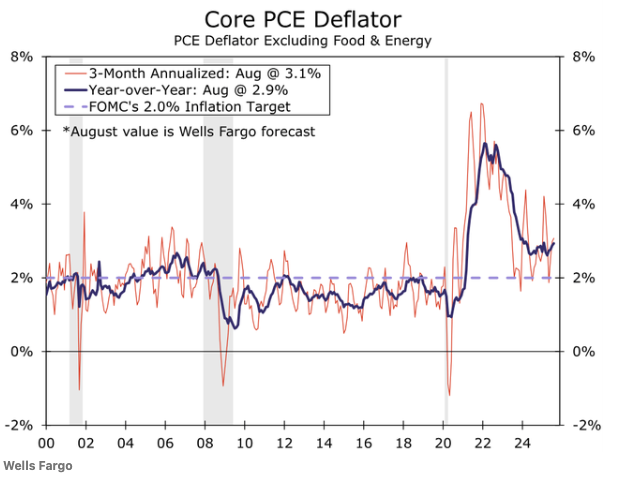

- Core PCE continues to trend higher, keeping inflation risk alive.

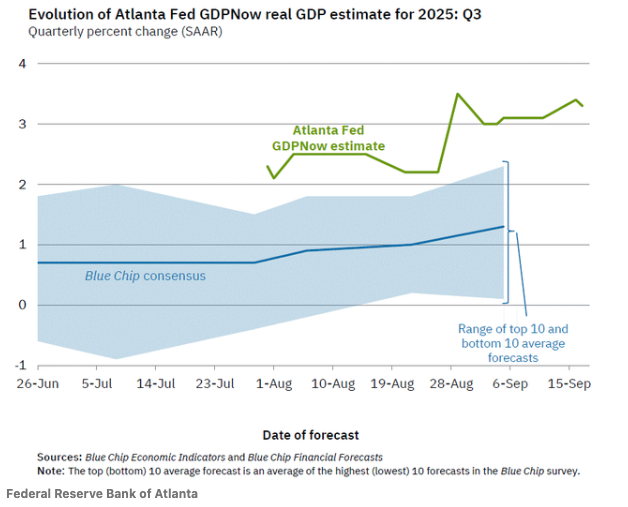

- Atlanta GDPNow suggests strong nominal growth despite soft patches in labour.

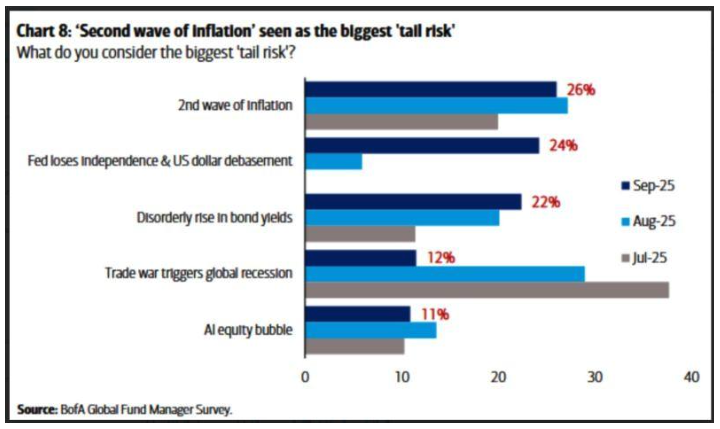

- Inflation tail risks remain a key concern for Q4.

Meanwhile, Trump is signalling warmer U.S.-China relations with the first U.S. House delegation to Beijing in six years, but the undertone remains protectionist with new visa fee hikes and persistent tariffs.

Technical & Sentiment Breakdown: Indices at Their Limits

Equity indices remain in uptrends but are stretched:

- Russell 2000 (R2k) outperformed SPX on rate-cut momentum, hitting its first new ATH since 2021.

- SPX valuation now at 3.3x quarterly sales — the highest in history.

- Nasdaq 100 is still trending up but showing early signs of exhaustion.

AI mega-caps dominate market cap: 109 AI stocks in the GS TMT basket are now worth $29.2 trillion, nearly matching U.S. GDP. This concentration magnifies both upside and downside risk — if the “Mag 7” stumbles, the entire index structure could wobble.

Gold and silver have ripped higher since the August pivot. Silver broke out of a textbook cup-and-handle pattern while gold hovers near short-term resistance, hinting at potential profit-taking.

Last Week’s Recap – Fed Fallout, Rising Recession Signals, and Gold Strength

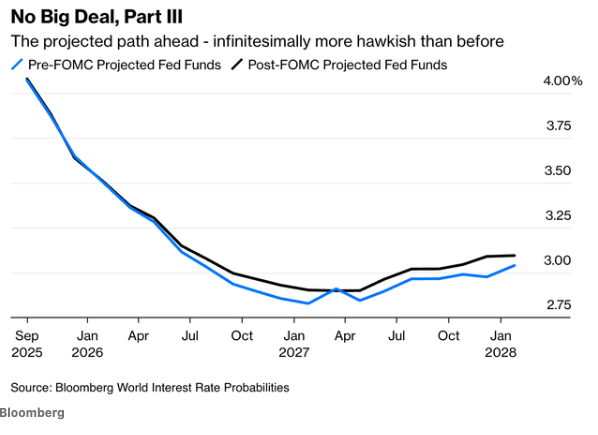

- FOMC Dot Plot: Turned more hawkish, even as markets priced in dovish outcomes.

- Treasury Yields: Jumped, with the dollar logging three straight days of gains.

- Gold Rally: Extended to five consecutive weeks, underscoring safe-haven demand.

- Labour Market: Disconnect between weakening job data and strong equity indices is widening.

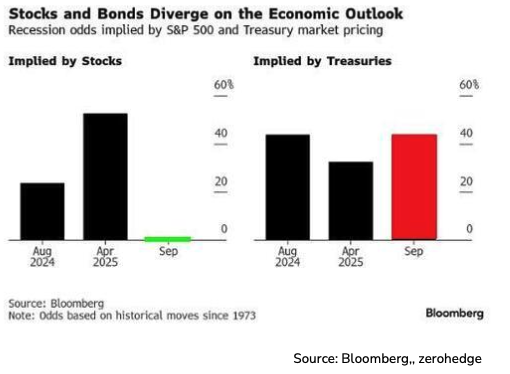

- Recession Indicators: Longview, bond markets, and JOLTS data flash warnings of a potential mid-cycle downturn rather than a full recession.

Global Developments

- BoJ announced earlier-than-expected plans to begin selling ETFs and JREITs, pressuring Japanese equities.

- Japan’s leadership race and renewed U.S.-China diplomacy added political noise but no immediate market impact.

The Week Ahead – Light Data, Heavy Signals

Monday, September 22

- Positioning flows dominate, with limited data releases.

Tuesday, September 23

- Micron earnings – critical read on semiconductors & AI hardware demand.

- U.S. Treasury auction (2Y).

Wednesday, September 24

- Speeches from Powell, Williams, Bostic, and Goolsbee – tone could sway rate expectations.

- U.S. Treasury auction (5Y).

Thursday, September 25

- Global PMIs – key gauge for manufacturing weakness and rate cut pricing.

- U.S. Treasury auction (7Y).

Friday, September 26

- Final U.S. GDP reading – expected to confirm stagflation setup.

- Costco earnings – retail demand snapshot heading into Q4.

Big Picture

It’s a light but pivotal week. With earnings thin and economic data limited, Fed speeches and bond auctions will dominate trading flows. The setup favours tactical fades and disciplined positioning ahead of a heavier October calendar.

Alpha Takeaway – Follow the Money, Respect the Pause

Markets remain constructive, but the risk of October’s volatility looms large. This is a tactical environment — the goal is to trade levels, not chase trends blindly.

Equities

- Indices are stretched with small caps leading, but Mag 7 concentration is a double-edged sword.

- Watch for rotations as October seasonality kicks in.

Gold & Silver

- Silver’s breakout remains bullish, but gold near $3,750 faces likely profit-taking in the near term.

Macro Focus

- PCE data and Treasury auctions are this week’s quiet catalysts — surprises here can reset rate expectations quickly.

Bottom Line for Traders

- Watch small caps vs. Mag 7 — they’ll set the market tone.

- Manage precious metals actively as momentum slows.

- Stay tactical and nimble — this is a market built for fades, not conviction longs.