Dot Plots, Gamma Flows, and Precious Metals in Overdrive

Markets closed September steady on the surface but fragile underneath. The Fed’s latest dot plot pushed expectations higher-for-longer, equities remain pinned by gamma flows, and gold and silver surged into overdrive. Beneath the calm, divergences in breadth, volatility suppression, and Treasury market stress suggest Q4 may not remain so quiet.

Market Overview: Calm Indices, Fragile Internals

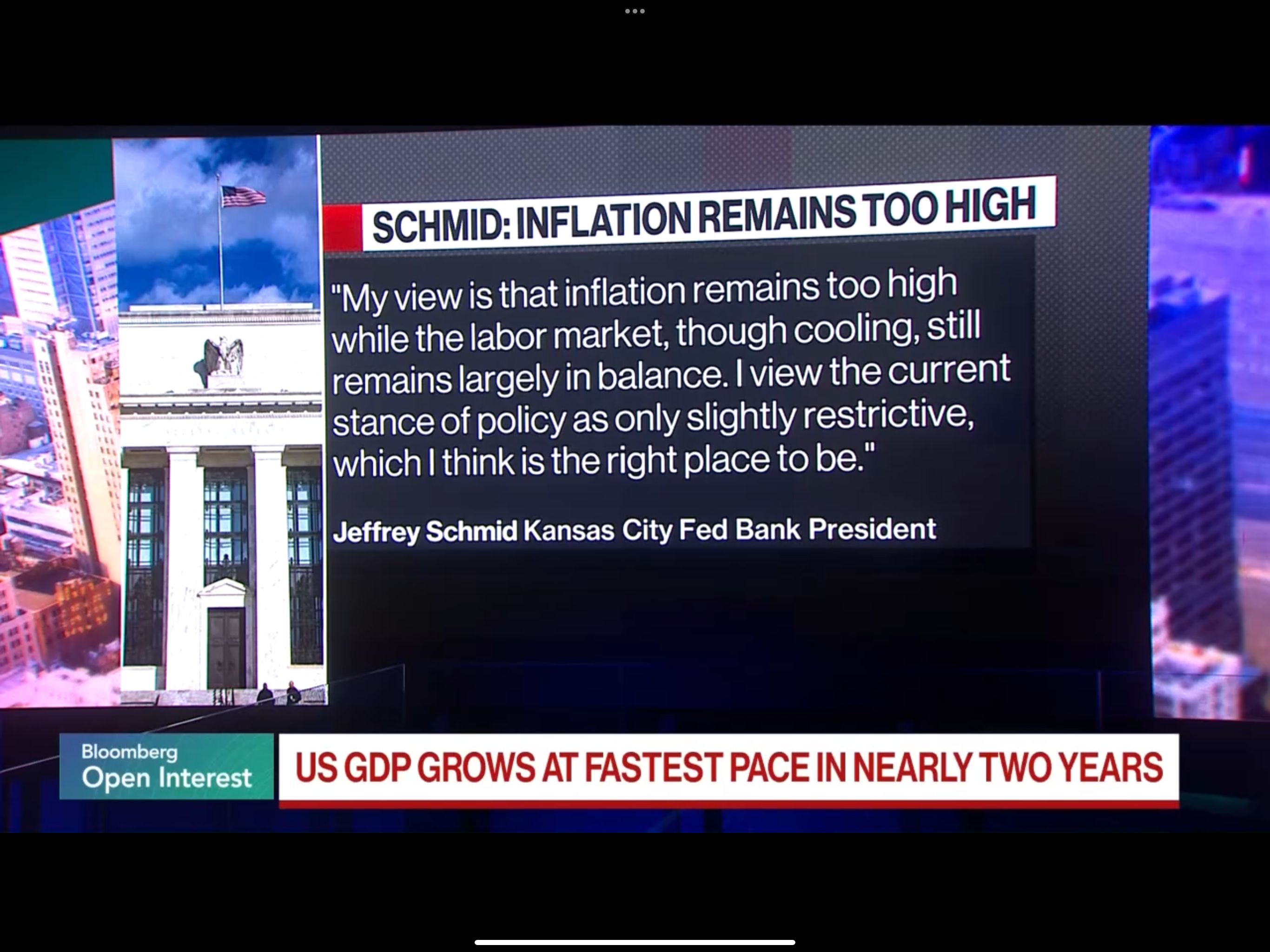

The Fed’s dot plot revisions confirmed what traders feared — policy makers are leaning hawkish, forcing markets to reconsider the “neutral” rate. Higher-for-longer has now been priced more firmly into expectations.

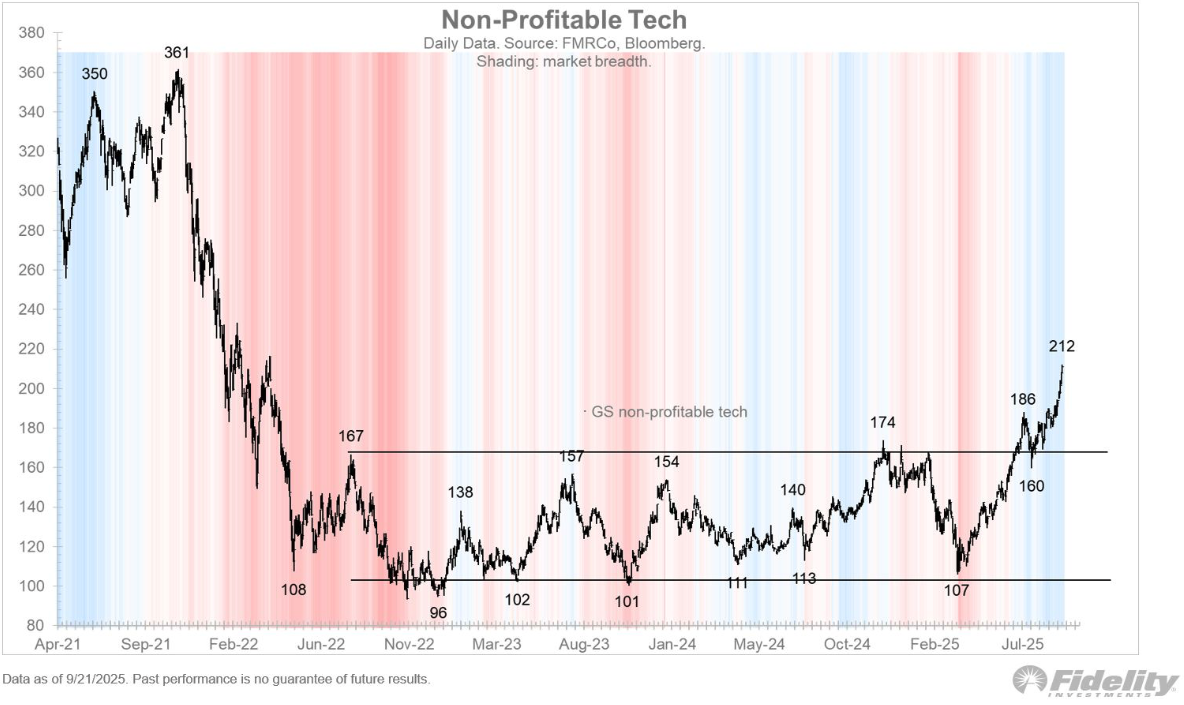

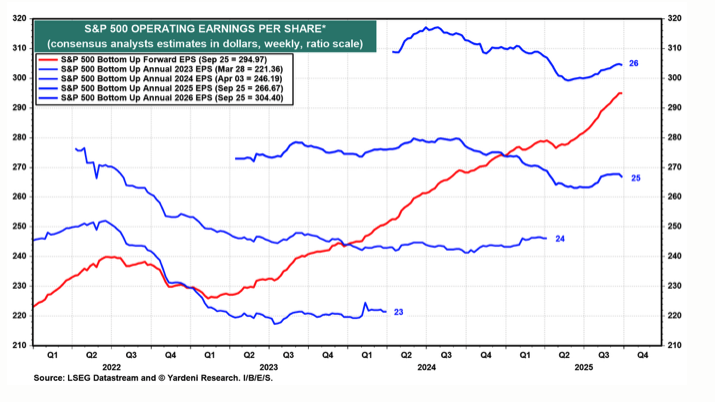

Equities continue their grind higher, but participation is narrowing. Mega-cap tech remains the driver, while non-profitable growth names weaken. Earnings resilience keeps the bullish case alive, but leadership is thin.

Globally, China’s tech rally offered support, yet U.S. Treasuries sent a different signal. Stress at the long end of the curve (10Y and 30Y) hints that bond investors aren’t fully convinced by the soft-landing narrative.

Macro & Policy Watch: Fed Hawkishness, China Momentum, Treasury Stress

The September Fed meeting delivered a clear message: the path to easing is shallower, and the definition of neutral has shifted upward. This structural adjustment means traders need to respect policy stickiness.

Meanwhile, China’s tech sector has regained momentum, breaking to multi-month highs. Policy tailwinds and investor flows into relative value plays supported the breakout.

But U.S. Treasuries tell another story. The 10Y and 30Y yields both highlighted ongoing supply-demand imbalances, weighing on investor sentiment.

Technical & Sentiment Breakdown: Gamma, Divergences & Commodities

NASDAQ 100 – Gamma Flows & Divergences

The NAS100 remains pinned near its gamma flip level. Options positioning shows heavy exposure at clustered strikes, raising the risk of outsized moves once hedging flows shift. Divergences between price and momentum caution against complacency.

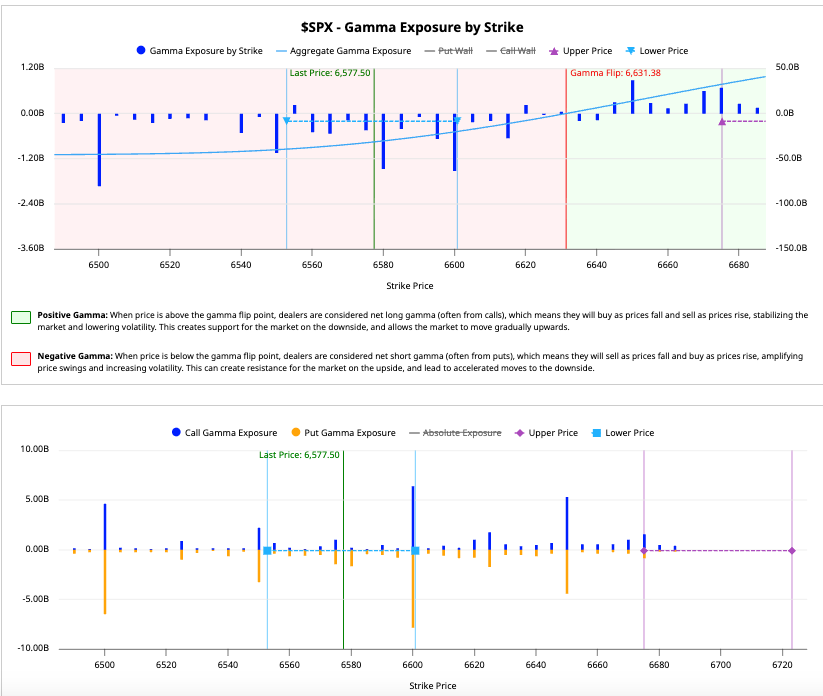

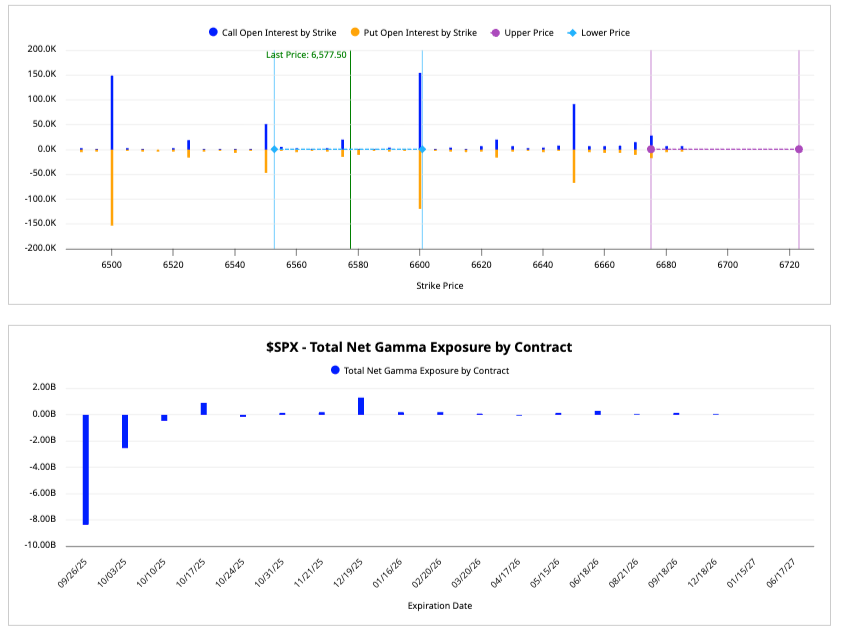

S&P 500 – Dealer Hedging Dominates

SPX intraday moves remain almost entirely dictated by dealer gamma flows. Until volatility reprices higher, expect chop around these mechanical levels.

Dollar & Options Positioning

The dollar trades tactically against global rate cut expectations. Options data shows traders positioning for asymmetric payoffs.

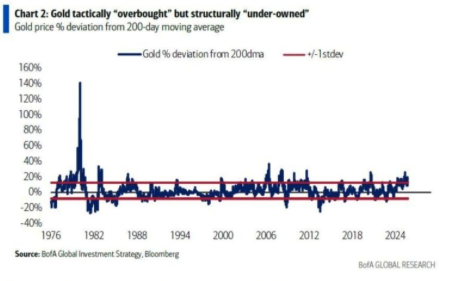

Gold & Silver – Overdrive Mode

Gold has broken to new all-time highs. While technically overbought, sentiment suggests it remains underowned — fuelling continued inflows. Silver is catching up rapidly, but now risks entering a blowoff zone.

Volatility – Too Quiet

Volatility indices remain unusually subdued despite macro risks. Traders should treat the calm as fragile — historically, suppressed vol often precedes explosive re-pricing.

Last Week’s Recap: Hawkish Fed, Strong Data, Metals Surge

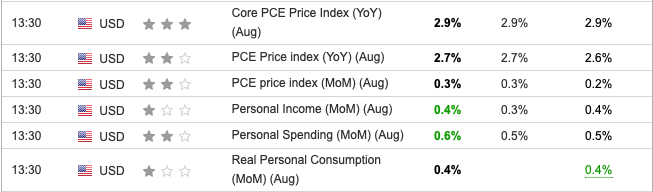

Inflation & Growth: A Mixed Pulse

- Core PCE remained firm, keeping the Fed cautious.

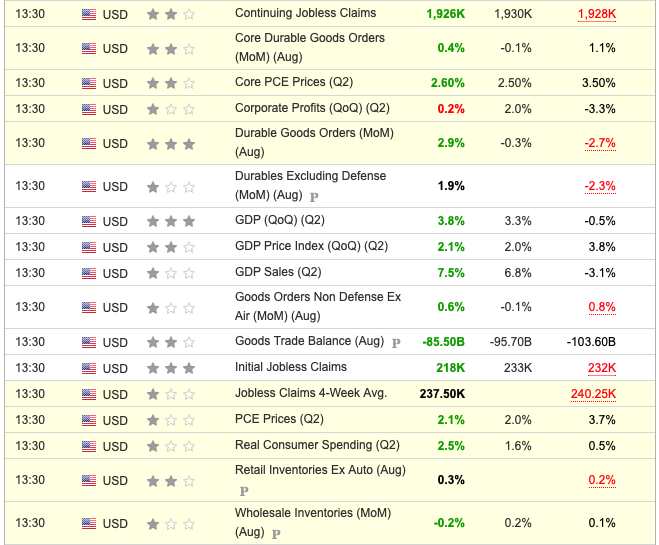

- GDP Q2 data pointed to resilience by the consumer, and Atlanta GDPNow surged to 3.9% for Q3, but cracks are forming at the margin with Michigan sentiment dropping and concerns about jobs growing.

Fed Speak: Hawkish Tone Dominated

- Policymakers reinforced higher-for-longer.

- Bond Markets priced fewer cuts and stickier inflation risks.

Earnings: Still Resilient

- Corporate earnings momentum continues, supporting valuations despite policy headwinds.

- Buy the dip saved the September rally from fading.

Metals: Relentless Bid

- Gold and silver rallied hard, extending their multi-week streaks.

The Week Ahead – Macro Data Cluster and NFP Spotlight

Monday 29th Sep 2025

- U.S. Treasury Bill Auctions

- ECB policymakers speaking

Tuesday 30th Sep 2025

- U.S. Consumer Confidence (key sentiment gauge)

- U.S. Housing Data

- Fed speakers providing post-FOMC guidance

Wednesday 1st Oct 2025

- Global PMIs & ISM Manufacturing (growth pulse checks)

- U.S. 10Y Treasury Auction (long-end stress in focus)

Thursday 2nd Oct 2025

- U.S. Jobless Claims

- ISM Services PMI

- ECB Minutes (cross-checking divergence with Fed stance)

Friday 3rd Oct 2025

- Nonfarm Payrolls (NFP), U.S. Unemployment Rate, and Average Hourly Earnings

- The most important release of the week, capable of resetting Fed expectations into Q4

Big Picture

Markets remain pinned by gamma levels, and volatility is suppressed. However, this week’s cluster of macro releases plus Friday’s NFP creates headline risk and potential intraday swings. Traders should maintain tight stops and disciplined levels. Friday in particular could trigger a volatility regime shift.

Alpha Takeaway: Fragile Calm, Volatility on the Horizon

Markets are holding together, but the calm is fragile. Beneath the surface, risks are stacking up:

Equities

- Earnings support valuations, but gamma-driven flows are masking thinning breadth.

Rates

- The U.S. 10Y and 30Y stress highlight unresolved fragility in the bond market.

Gold & Silver

- Strong momentum persists, but silver in particular risks blowoff behaviour.

Volatility

- Still at compressed levels, leaving traders exposed to sudden shocks.

Our Stance

- Respect gamma flip zones in SPX and NASDAQ; chasing extended rallies is dangerous.

- Stay tactical and defensive, tighten stops on equity exposure.

- Use gold/silver strength strategically; partial profit-taking is prudent before blowoff phases.

- Position ahead of NFP for a potential volatility regime shift.

=