Fed Cuts, Gold Breakouts & September’s Seasonal Chop

Markets stumble into September—the seasonally weakest month—caught between softening labour data, Fed cut speculation, and commodity breakouts. Traders are weighing whether “bad news is good news,” but volatility looms large as macro cracks widen.

Market Overview: Flat Jobs, Rising Risks

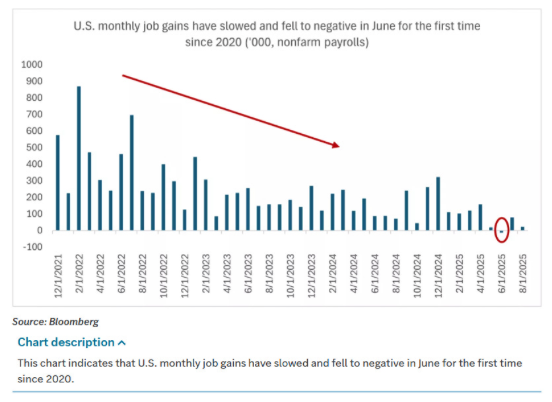

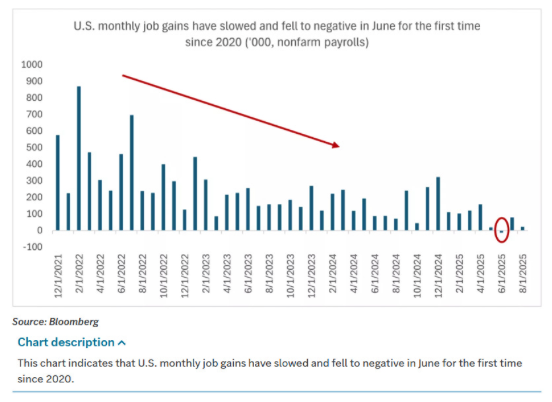

Friday’s jobs data rattled sentiment. June was revised negative for the first time since 2020, while July’s downgrade erased August’s modest +22k gain. Net impact: the labour market is flat.

Equities initially popped but quickly sold off, underscoring the market’s indecision. Retail optimism clashes with institutional caution—positioning is light, but volatility is creeping.

Key Market Signals

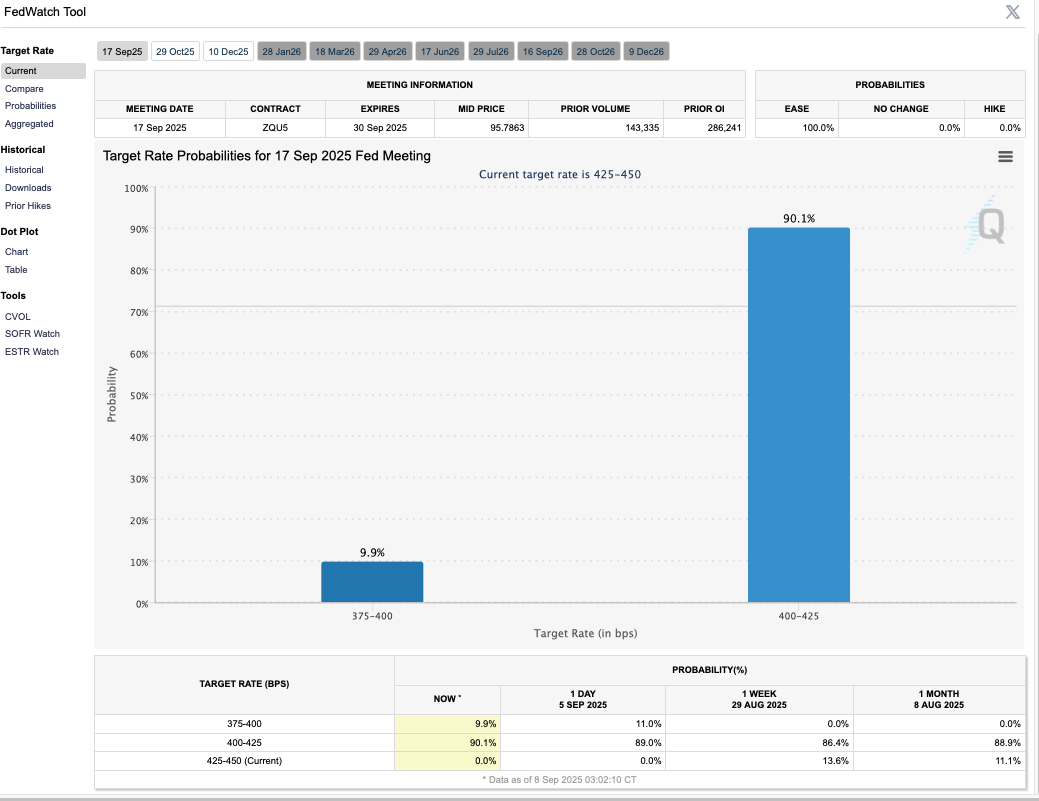

- Fed odds shift: 10% chance of a 50bp cut this month, consensus remains 25bp in September and October

- Gold surges to fresh ATHs, but short-term momentum looks stretched

- Oil’s “glut” narrative is cracking—supply could tighten fast

- Equities remain in uptrends, but corrections are likely before Q4 catch-up

Macro & Policy Watch: Fed Behind the Curve

The Fed is back in focus. Last week’s jobs data confirms a deterioration that Powell can use as cover for easing. But the debate is not about when cuts begin—it’s how much.

Fed Expectations

- Market expects 3–4 cuts by year-end, totalling 75–100bps

- The risk: a 50bp “panic cut” spooks confidence, triggering outflows despite equity optimism

- Consensus: 25bp September, 25bp October, but the Fed has a history of moving decisively once it starts cutting

Global Watchpoints

France

Another confidence vote looms, keeping capital outflows in play.

Japan

Ishiba’s exit tilts policy dovish, raising spending expectations.

UK

Labour’s anti-growth policies risk driving capital flight, though GBP holds steady near $1.335–1.360.

China

CPI/PPI data Wednesday—deflationary prints could force stimulus; disappointment may trigger risk-off.

Technical & Sentiment Breakdown: Key Setups

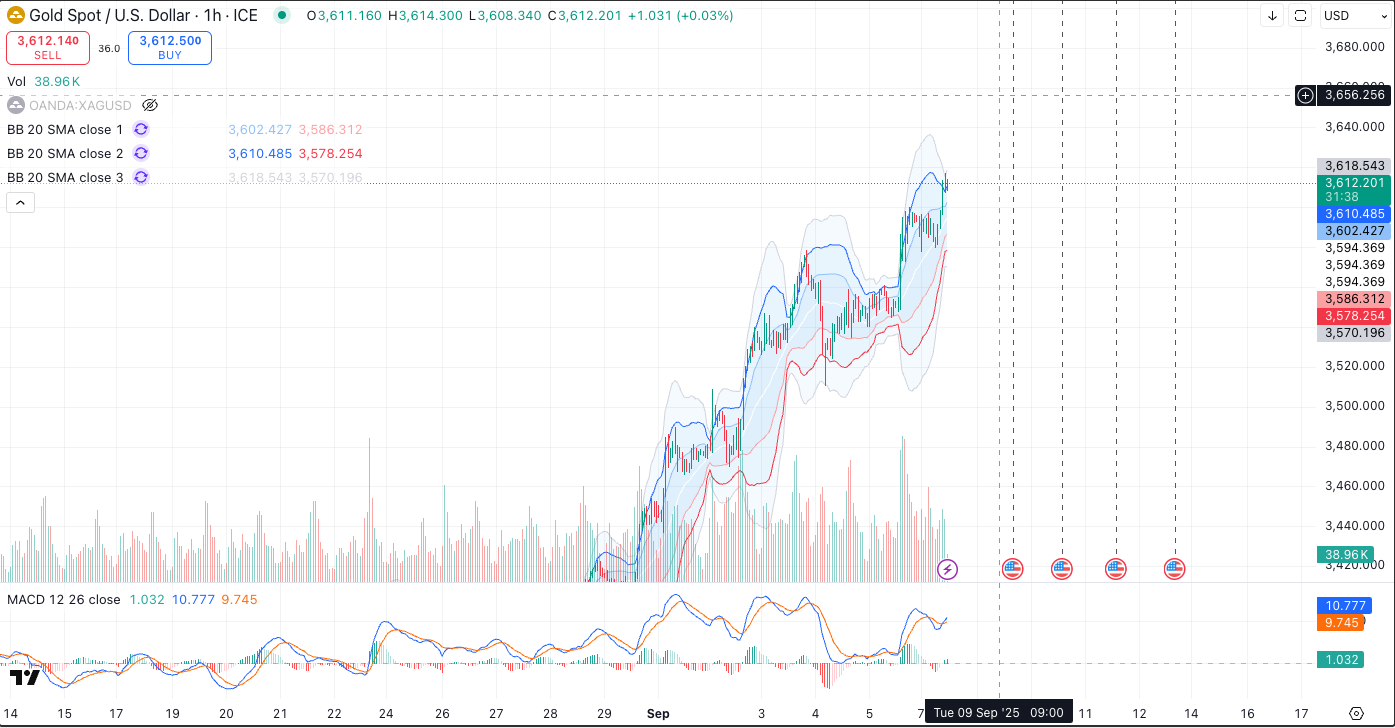

Gold – Breakout Confirmed, but Overheated

Gold has smashed into a new ATH, confirming the impulse wave breakout we flagged months ago. Seasonality (India, Christmas, China) plus macro drivers (weak dollar, safe-haven demand, fiscal expansion) reinforce the bullish case.

- Medium-term target: $4k by year-end

- Short-term: Price is hugging Bollinger Bands, with fading MACD momentum

- A pullback is overdue

Oil – Supply Story Flips

Talk of oversupply masks deeper tightening pressures. Russia’s sanctions and China’s strategic reserve building drain supply, leaving Saudi Arabia as the only true swing producer.

This setup risks a commodity breakout that could reintroduce inflationary pressures by 2026.

NAS100 – Wave (4) Consolidation in Play

The August top played out as expected, with last week’s rejection reinforcing the wave (4) pullback narrative.

- 38.2% Fibonacci retrace looks like the probable termination level

- Aligns with seasonality

- Alternative setup opens if ATHs are breached

Volatility – Calm Before the Spike

Both MOVE and VIX remain subdued, suggesting a “wait and see” market. But any downside will likely be driven by a MOVE spike, bleeding into equity volatility.

Last Week’s Recap: From Jobs to Jitters

NFP

- Net zero growth after revisions

- June marked the first negative print since 2020

Equities

- Friday rally faded

- Fed seen as behind the curve

Commodities

- Gold breakout delivered, with fresh ATH momentum

- Oil conflicting narratives intensify—oversupply vs tightening

Volatility

- Held steady, but traders braced for spikes

The Week Ahead: Inflation & Central Banks

Monday, Sep 8

- Quiet open

- Positioning carries over from NFP shock

Tuesday, Sep 9

- US NFP benchmark revision

- Last year’s came in at -598k; a large negative could shake confidence

Wednesday, Sep 10

- China CPI/PPI — all eyes on deflationary pressures and policy response

- US PPI — tariff impacts and services inflation in focus

Thursday, Sep 11

- US CPI — the marquee release; softer prints revive 50bp cut debate

- ECB rate decision — expected on hold, hawks and doves split

Friday, Sep 12

- Eurozone final CPI — confirmation data for the ECB

- UK GDP/activity data — slowdown from June’s upbeat surprise expected

- UoM surveys & inflation expectations — key sentiment wrap to close the week

Alpha Takeaway: Trade the Chop, Don’t Fear It

The Fed is boxed in—cuts are coming, the only question is pace. Equities remain in uptrends, but September chop is real. Expect selective opportunities rather than broad melt-ups.

Our Stance

Equities

Buy The Dip within channels, but keep stops tight.

Gold

Long-term bullish, short-term stretched—don’t chase highs blindly.

Oil

Supply squeeze brewing; watch Saudi rhetoric.

Volatility

Likely to dictate trade entries and exits in the coming weeks.

September is about nimble trading, not conviction plays. Stay flexible, avoid bias traps, and use the chop to your advantage.